It’s an incredible time for high school seniors. The SAT and ACT are behind them. College applications are done. They’re looking at their last semester of high school and are going be the center of attention for their families over the next few months. It’s one of those special times in a person’s life.

For most of them, they’re finding out that they worried about a lot of things for their college applications last summer and into the fall for nothing. They’ve got 3 or 4 or more good college acceptances in hand. Now the hard part is deciding which one is right. For the record, there is no such thing as 1 right choice.

But there can be such a thing as a wrong choice.

Along with those acceptance letters, students and their families are finding out how much that dream school is actually going to cost. And the cost can be shocking.

A dose of reality

For many families, it seems inherently unfair. The student played by the rules. They followed the recipe that society laid out. Work hard. Do your homework, take tough classes, be involved, and you’ll get to go to your dream school.

Scrolling through social media, I came across an interesting discussion along these lines. A hardworking student had gotten into Michigan, a fantastic honor. Now the family was looking at the financial statement from the university.

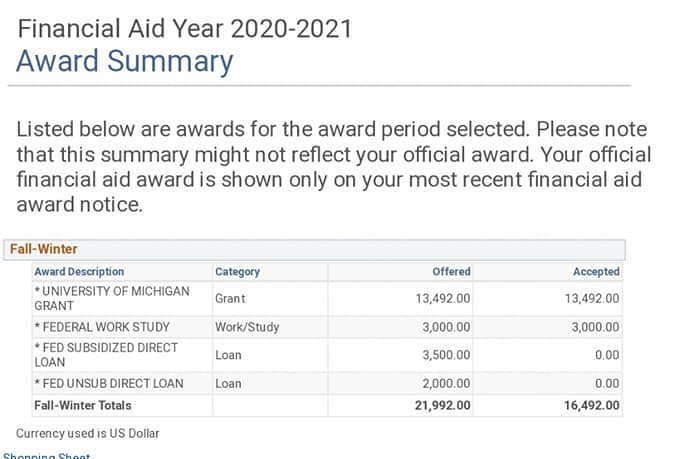

At first glance, it looks kind of like the school is offering about $22k in financial aid. Then come the “excepts”.

- except it includes $5500 in federal loans

- except it has $3000 in “work/study” which isn’t guaranteed and goes straight to the student, not to costs

- except it still leaves about $9000 to cover

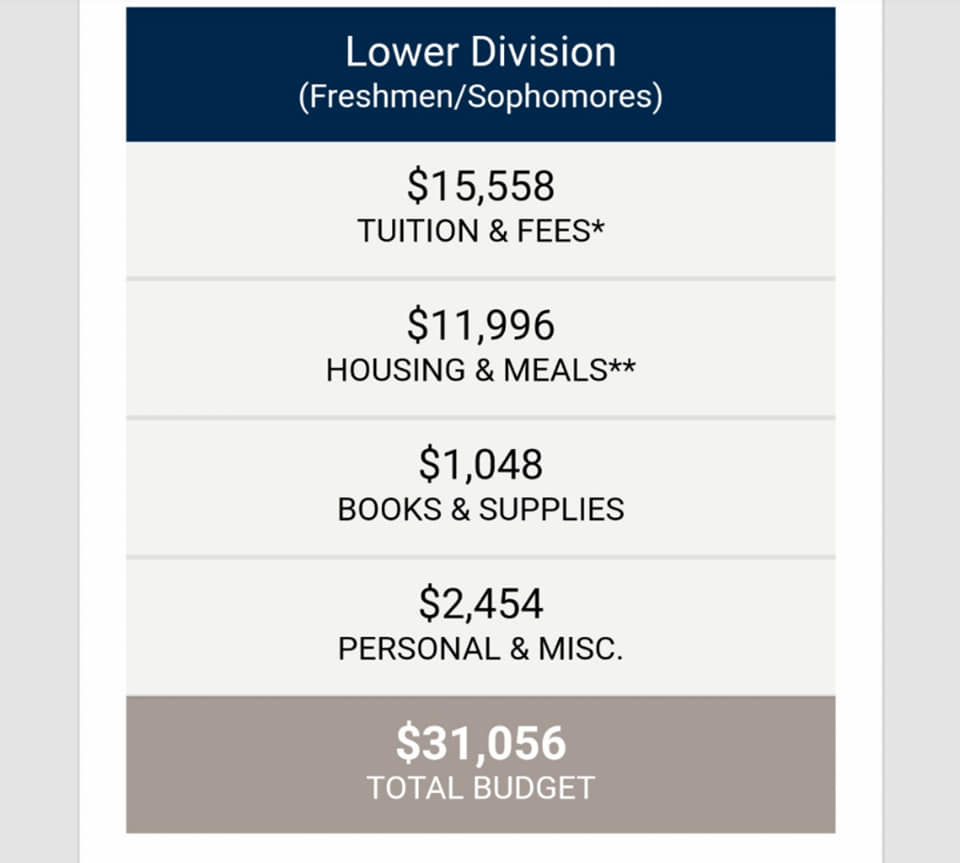

Included with the financial award was the university’s estimated costs.

They estimate it will cost $31k to attend for the year. The $22k award already doesn’t cover $9k of the estimated costs. Then it includes $5500 of debt and $3000 of a possible work/study job? The family and student are still going to need to come up with $12k per year ($9000 gap plus the $3000 work/study).

What that means

Federal loans are capped at $27,000 for a student. $5500 as a freshman, $6500 as a sophomore, and $7500 for juniors and seniors. It’s become more typical for students to max out these loans, and graduating with a college degree and $27,000 in debt isn’t catastrophic. It will mean about a $300 a month payment for the student after graduation, but it’s doable.

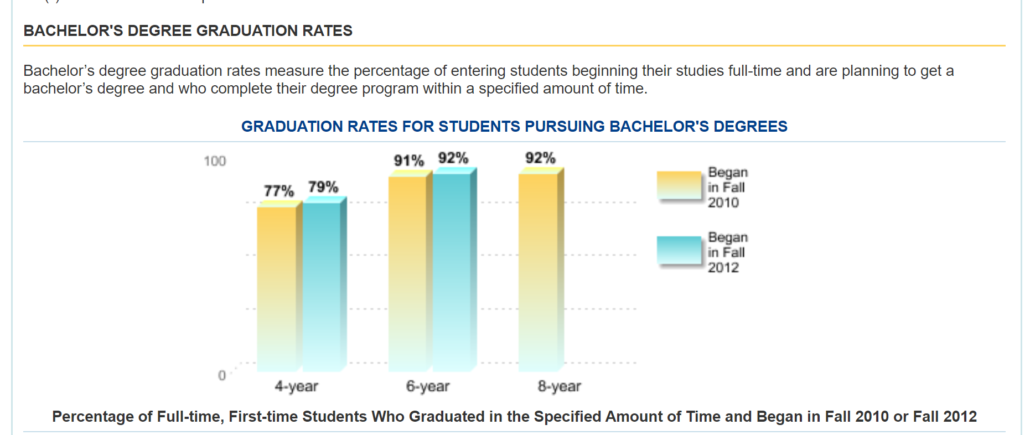

Thankfully, according to College Navigator, Michigan has a 4-year graduation rate of 79%.

according to College Navigator, 28 Jan 20

The student is highly likely to get that degree in 4 years, so the family and student are looking at a $48k shortfall. That’s if everything is perfect.

If the family was able to save $48k over the years so the student has a college fund, great. Or maybe the student can take on a summer job that will help with some of the difference. It’ll be tough, but again, doable. But over and over families and students are willing to take out loans on the promise of a college degree and a great job.

The hard truth

It’s a tough conversation, but there are likely other, better options. At first it probably seems unfair. The student did all the right things. Isn’t the reward supposed to be going to the school of their dreams?

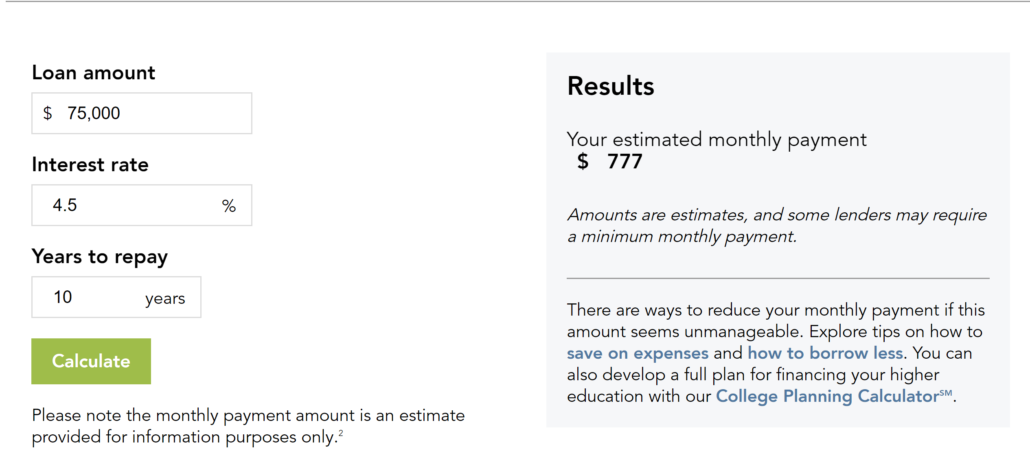

When they graduate with $75,000 of student debt ($48,000 gap plus the $27,000 federal), the dream becomes a nightmare.

Using Sallie Mae’s calculator, that’s a $777 per month payment over 10 years.

It’s a tough conversation to have, but it has to be done.

Expenses and savings

At our College App Camp, we have that tough talk with students on the last day of the camp. We show them that the average salary for a college graduate is $48,000.

$4000 a month minus the 25% that the government takes from the start leaves $3000. The average 1 bedroom apartment in our area is at least $1000. They’ve got $2000 left.

Thank goodness mom and dad still have them on the insurance and the cell phone plan. Even if they are “sharing” logins for Netflix and Hulu, they’re going to want WiFi at the apartment. $50 a month? Electricity, gas, water? Budget another $150. $300 a month for groceries. $50 a weekend for things like happy hours and socializing. $200 most months. Gas for the car? $100 if they’re driving a hybrid.

That’s $800 in monthly expenses, and we’re just scratching the surface. We haven’t furnished the apartment. Knowing they’re looking at $800 a month in student loan payments, they’ve got about $400 a month to buy clothes, a couch, a television, a bed, not in any particular order. That’s if the car doesn’t break down or something else goes wrong. And they aren’t exactly socking it away for a down payment on a home, not that they could get a loan with $75,000 of unsecured debt on their credit report.

Some families will turn to Parent PLUS loans. These are even worse. If the family wasn’t able to save for college over the years, it’s likely they’ll have problems qualifying for the loans. If they do qualify, the interest rates will be higher, forcing parents to bear a debt burden that they may not have the earning years to support.

Better options

Students have tons of better options. One is taking advantage of the lower cost options. I talk to students regularly who tell me they’re wanting “the college experience”. I explain that every college has an experience. What they need to focus on is finding a place where they can be a rock star. That’s going to be a much better investment that mortgaging their parents’ futures or signing up for $75,000 in debt before you’re 22.

Maybe that means 2 years at the community college. Maybe that means commuting to attend the local public university. But it has to mean avoiding unsustainable levels of debt.

It’s a tough conversation that families will have to have along with the celebrations this Spring, but it’s a conversation that is worth having.